OVERVIEW

The U.S. stock market slipped further into negative territory last week, as the S&P 500 fell 2.75%, the Dow Jones Industrial Average dropped 1.86%, and the Nasdaq Composite tumbled 3.83%.

Investors didn’t find much safety in bonds last week, as the yield on the 10-year Treasury note rose to 2.917%, up from 2.83% the week before. Long-term Treasuries dipped 0.59%, and investment-grade corporate bonds slipped around 1.4%. High-yield (junk) bonds, which tend to act like equities, fell around 0.88%. Only inflation-protected Treasuries (TIPS) saw positive returns for the week, gaining around 0.21% after real yields dropped slightly after briefly rising to 0% mid-week.

As for foreign stocks, they didn’t hold up any better. Developed country stocks fell roughly 1.6%, and emerging markets plummeted about 3.35%. The U.S. dollar strengthened by about 0.82% and is up roughly 5.5% year to date.

Commodities traded lower on the week, dropping around 2.5% overall. Oil fell 4.1%, gold dropped 2.06%, and corn rose slightly by about 0.67%.

Option-implied volatility is down from the March high but remains somewhat elevated as the VIX continues to trade above 20—a sign that investors remain skittish toward the stock market.

KEY CONSIDERATIONS

The Biggest Losers – When we model stock market risk, we break the analysis down into three major categories: Price Movement, Investor Behavior, and the Economic Environment. Each of these categories can be further broken down into six sub-components, for a total of 18 sub-components or composites that we feel most closely characterize the risks pertaining to the stock market.

If you were to ask me which of these 18 sub-composites have been the weakest so far this year, I’d have to point to either the Inflation Composite or the Interest Rate Composite.

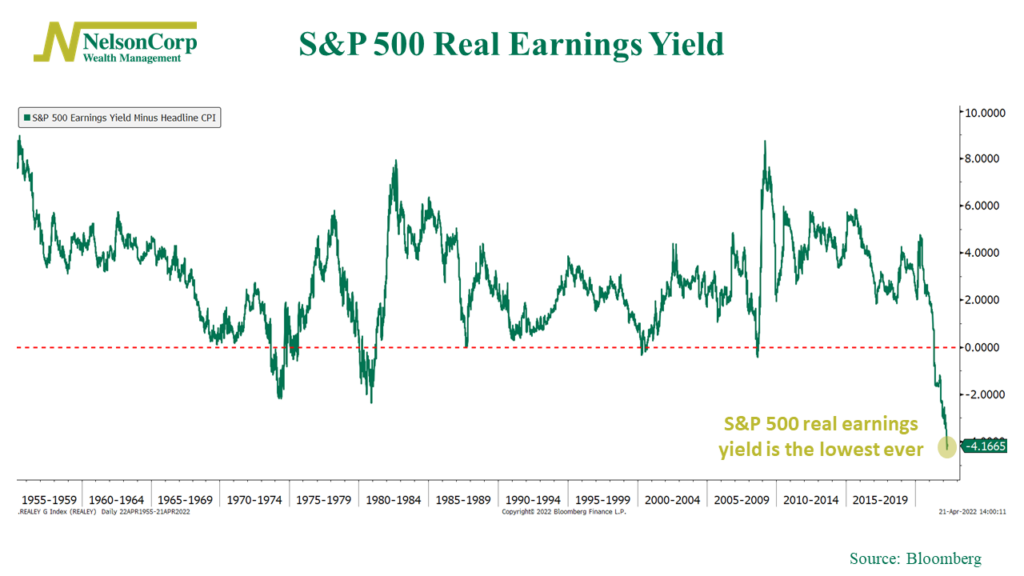

First, let’s talk about inflation. Inflation is problematic for stocks for various reasons, but here’s one way of visualizing the risk. The chart below shows the earnings yield of the S&P 500 minus the headline CPI. In other words, it shows what the companies in the S&P 500 are generating in earnings relative to their stock price after taking inflation into account.

We call this the real earnings yield of the stock market. As you can see, it’s at its lowest point in the entire history of the data, going back to 1955.

You might also notice that it’s negative. The last three times this happened—1987, 2000, and 2008—the market went on to decline by more than 20%. So, the fact that the market has been somewhat resilient in the face of a record-low real earnings yield could be one reason to be bullish. Alternatively, from a bearish perspective, it could just be an anomaly waiting to be corrected once monetary accommodation is no longer so, well, accommodative.

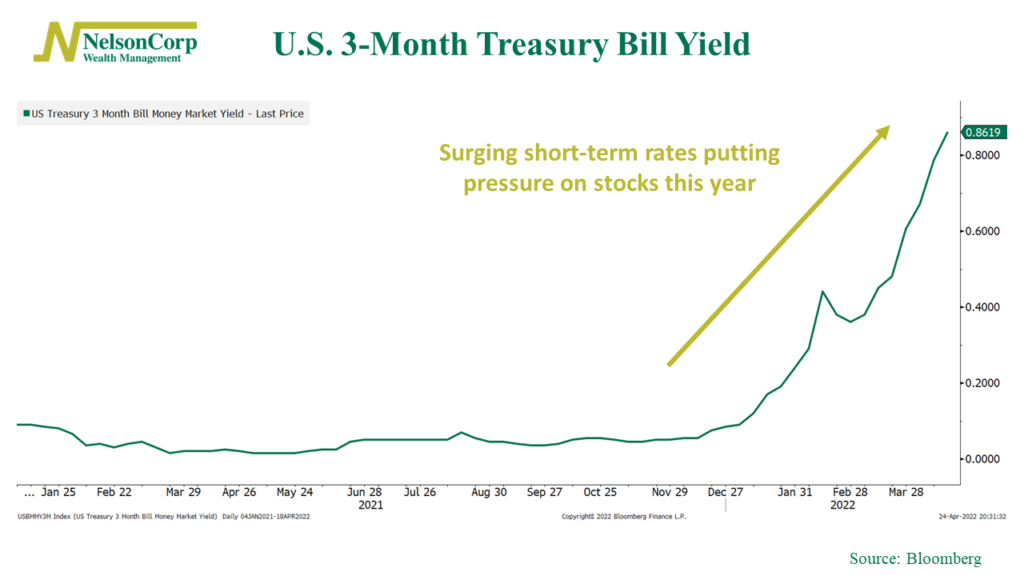

This brings up the next big issue: interest rates. The side effect of high inflation is rising interest rates. And rising interest rates put pressure on stock prices. This has arguably been the biggest drag on the stock market this year.

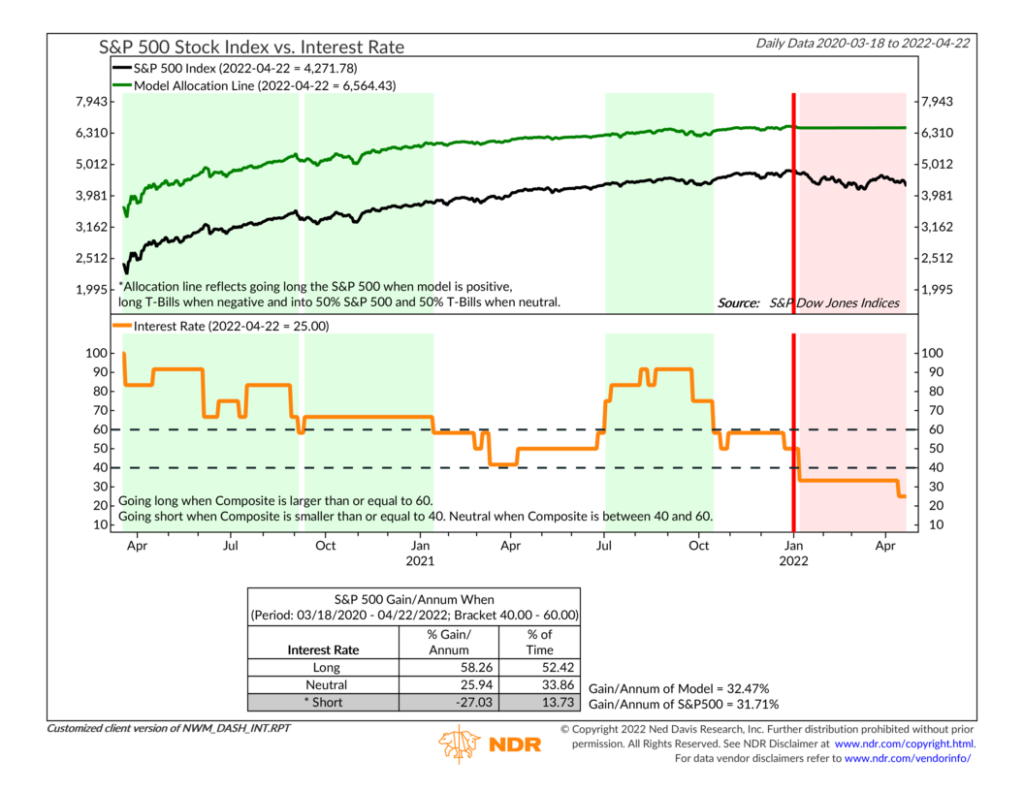

Here’s a chart of the Interest Rate Composite, with the red line denoting the start of 2022. As you can see, the model (orange line) fell into negative territory at the beginning of the year, and it isn’t showing signs of getting better anytime soon.

In fact, it’s probably about to get worse.

Of the six indicators that make up the Interest Rate Composite, four are negative, one is positive, and one is neutral. The neutral one is a measure of short-term interest rate momentum, and due to the massive surge in 3-month Treasury Bill yields this year, it looks set to turn negative any day now.

So, the bottom line is that if you’re wondering why stocks have struggled so much this year, the biggest losers—inflation and interest rates—go a long way towards explaining a lot of it.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The post The Biggest Losers first appeared on NelsonCorp.com.