OVERVIEW

U.S. stocks were mixed last week, as the S&P 500 climbed 1.62% and the Nasdaq surged 3.31%, but the Dow fell about 0.15%.

Growth stocks lead the rally, rising roughly 2.8%, versus a 1% gain for value stocks. Small-cap stocks outperformed, climbing nearly 5%.

Foreign stocks were also mixed. The MSCI EAFE index of developed country stocks rose 0.46%, while the MSCI EM index of emerging market stocks dropped about 1.2%.

Returns were also mixed over in the bond market as the 10-year Treasury rate remained roughly flat at around 3.5%, despite dropping to under 3.4% at one point during the week. Short-term Treasuries rose 0.07%, intermediate-term Treasuries fell 0.06%, and long-term Treasuries gained 0.2%. Investment-grade corporates rose 0.3%, and high-yield (junk) bonds gained 1%. Municipal bonds dropped 0.08%, and TIPS fell 0.85%.

Commodities were down big for the week, with the broad-based index down over 4%. Oil declined 7.3%, gold fell 3.55%, and corn dropped 0.81%. However, real estate was up 1.77%, and the U.S. dollar climbed 1.16%.

KEY CONSIDERATIONS

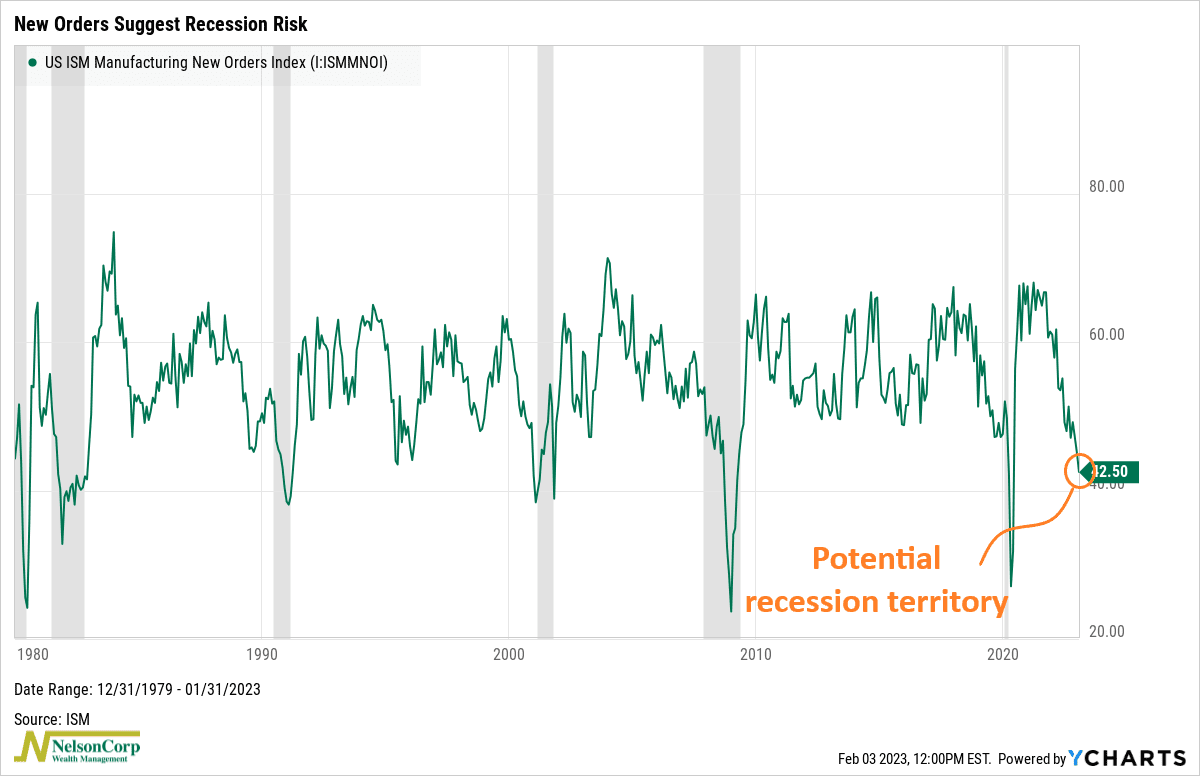

Balancing the Risks – When we look at the external factors that affect the stock market, there is no doubt there are still a lot of risks out there. For example, ISM Manufacturing New Orders, shown below, have dipped into a territory that suggests an economic recession is a real possibility.

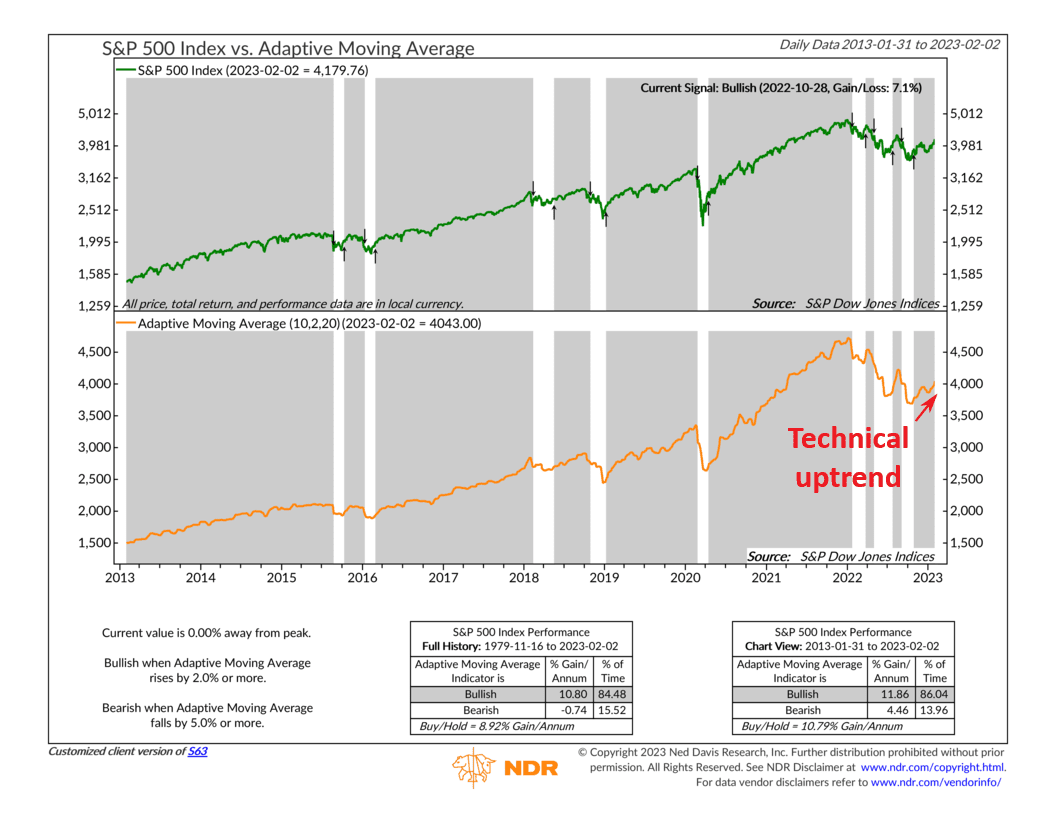

However, it’s hard to ignore the fact that stock market momentum has been strong lately. The S&P 500 Index—an index of the 500 largest stocks in the United States—climbed over 6% in January. What’s going on?

Well, for one, an adaptive moving average indicator, shown below, suggests that the S&P 500 Index has been in a technical uptrend since the end of October.

This indicator is designed to account for market noise or volatility and adapt to changing conditions; therefore, a positive signal is a credible sign of market momentum.

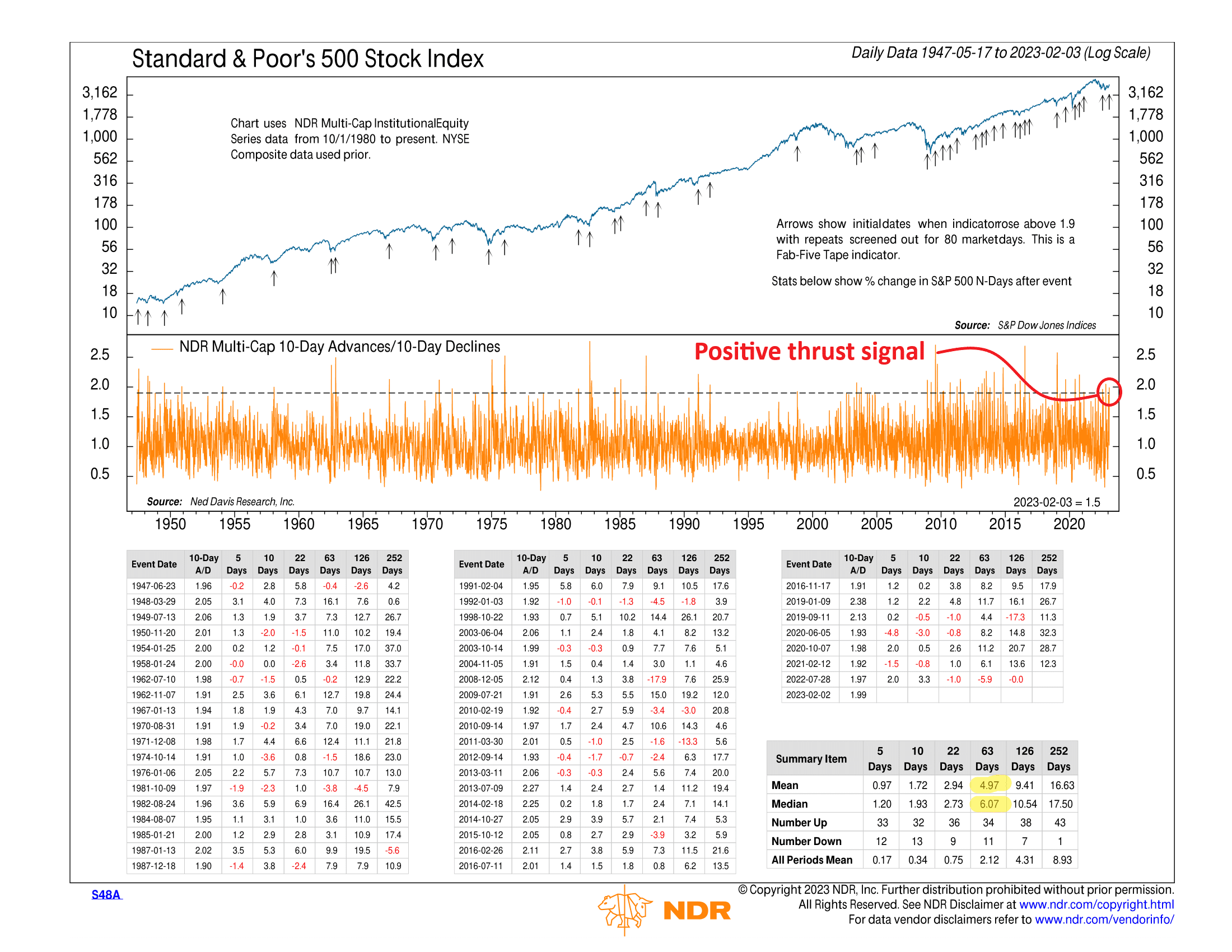

Adding to that, we’ve recently received a plethora of positive signals from various “thrust” indicators.

One of them—the McClellan Summation Index—was highlighted as the featured indicator this week on our blog. It basically says that the number of advancing stocks is outpacing the number of declining stocks to such a degree that higher stock market returns tend to follow over the next three months to a year.

Backing this up is another thrust indicator, shown below, that recently gave a positive signal. It suggests that the number of advancing stocks has outnumbered declining stocks by such a wide margin over a 10-day period that a significant shift in market momentum has occurred. On average, the S&P 500 returns roughly 5%-6% over the next three months after a positive signal from this indicator.

So, despite the risk of a potential recession or just a general slowdown in economic growth, the stock market appears to be shaking those risks off.

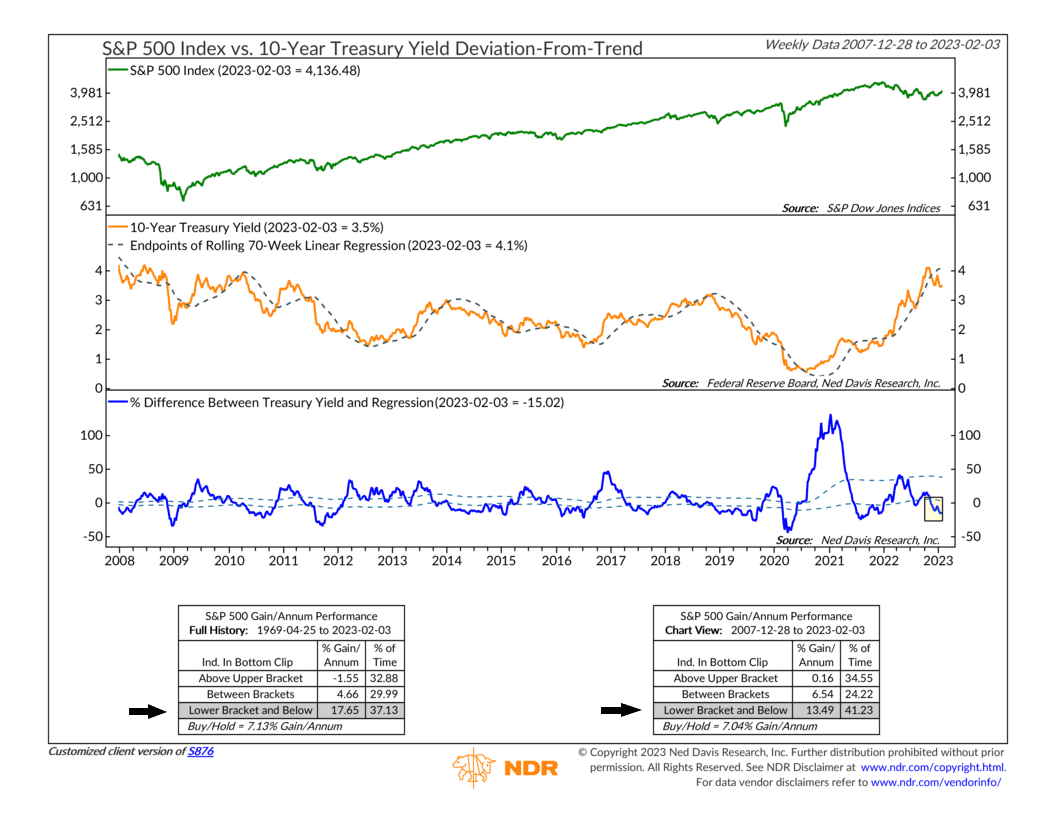

For it to last, we’ll look for continued evidence that inflation has peaked and that, in turn, interest rates have also peaked.

The good news is that, according to the indicator below, 10-year Treasury rates have stopped climbing and recently settled into a zone that has historically been the best environment for stronger stock market returns.

The bottom line? While we certainly wouldn’t say that our current view is strongly positive, we think that holding some additional exposure to risk assets is prudent at this time—given the factors discussed above.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The post Balancing the Risks first appeared on NelsonCorp.com.