OVERVIEW

The major U.S. stock market indices were mixed last week, as the S&P 500 fell 0.43%, the Dow dropped 0.51%, and the Nasdaq climbed 0.31%.

Growth stocks ended the week positive, gaining about 0.14%, whereas value stocks fell around 0.7%.

Things looked much better on the international front. Developed country stocks rose 0.98%, and emerging market stocks gained 1.72% for the week.

Bonds had a modestly good week as interest rates ticked down a bit. Long-term Treasuries gained 0.47%, investment-grade corporate bonds rose 0.18%, and municipal bonds edged slightly higher by about two basis points. However, high-yield (junk) bonds sold off by about 0.09%, and inflation-protected Treasuries (TIPS) fell around 0.34%. Emerging market bonds also declined in both U.S. dollar and local currency terms.

Returns were mixed in the real asset space. Real estate gained about 0.82% for the week. Commodities, however, fell around 1.18%. Gold and corn actually did well, gaining 2.11% and 2.45%, respectively. Energy was down, however, as oil fell 2.26%.

And finally, the U.S. dollar ticked lower by about 0.3%.

KEY CONSIDERATIONS

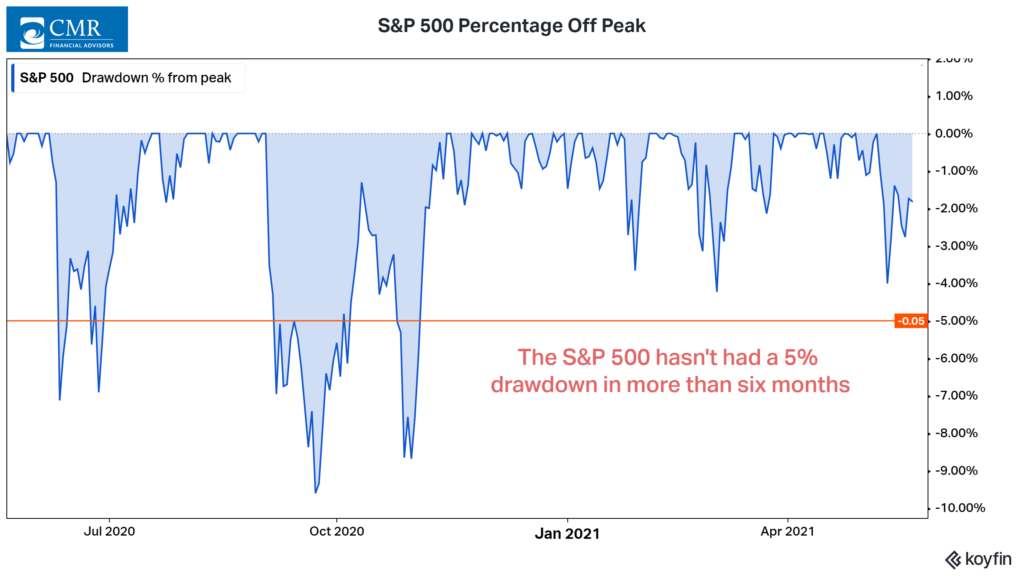

On Edge – U.S. stocks have hit a rough patch recently, trading flat or sideways for about a month now. By many measures, momentum has faded—particularly when compared to the phenomenal price action earlier this year and late last year.

But perhaps it makes sense that things have cooled off. The S&P 500 index of large-cap stocks hasn’t seen a correction of 5% or more since November of last year, as the chart below illustrates. And the farthest the index fell from its peak in this most recent bout of weakness was about 4% about a week and a half ago.

Of course, the selling might not be over. Stocks could absolutely see a correction—defined as a 10% or more decline from recent highs—before the year is up. But this would probably be welcome since it would likely wash out some of the excessive optimism we’ve witnessed recently in the market. In fact, some of this has happened already: The number of “bulls” in the American Association of Individual Investors (AAII) survey has fallen from 70% a month ago to just under 60% today.

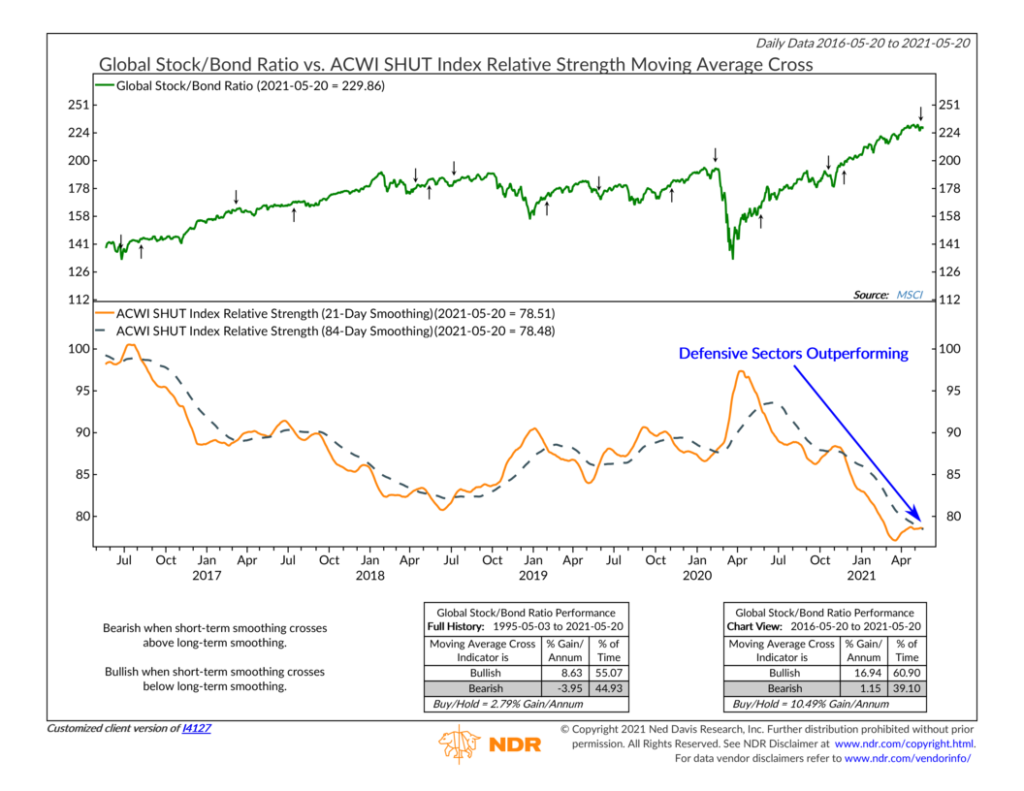

With that said, however, we don’t want to be blind to the risks forming in the market. The story so far this year has been the ongoing rotation out of the high-flying growth sectors of the stock market and into the more economically sensitive value-type sectors. Recently, though, we’ve seen defensive-type sectors of the market outperform.

For example, the chart below plots the ratio of the ACWI SHUT Index to the ACWI ex. SHUT Index. The SHUT index is a composite of the Consumer Staples, Health Care, Utilities, and Telecommunications sectors. These sectors have historically been considered defensive given their low volatility relative to stocks overall. Therefore, when the relative strength line (its technical name) rises far enough, it triggers a sell signal for the broader stock market.

We got this warning sign about a week ago, suggesting that investors are positioning themselves more defensively. This will be something to watch going forward in conjunction with the rest of our indicators, many of which have recently deteriorated to a more neutral but still slightly bullish level.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The post On Edge first appeared on NelsonCorp.com.