OVERVIEW

Last week, the S&P 500, Dow Jones Industrial Average, and Nasdaq Composite all saw negative returns, with the Nasdaq experiencing the largest drop at -2.72%. The Dow fell -1.66%, and the S&P 500 decreased -2.08%. The VIX Index, which measures market volatility, also saw a slight decrease of -0.92%.

In foreign markets, the MSCI EAFE Index of developed country stocks and the MSCI EM Index of emerging market stocks both saw similar declines of roughly -2.14%.

In terms of bond indices, intermediate-term Treasuries and long-term Treasuries both saw positive returns, with long-term Treasuries experiencing a slightly larger return of +0.92%. Investment-grade corporate bonds registered a small increase of +0.55%, while both high-yield (junk) and municipal bonds saw minimal increases of +0.03%. TIPS, or Treasury Inflation-Protected Securities, realized a negative return of -0.78%.

The real estate market was down about -2.03%, while commodities as a whole saw a slight increase of +0.87%. Oil saw a significant increase of +3.26%, but gold saw a slight decrease of -0.58%. Corn had a positive return of +1.4%, and the U.S. Dollar decreased slightly by -0.18%.

Overall, it was a mixed week for financial markets, with some sectors seeing positive returns and others experiencing declines.

KEY CONSIDERATIONS

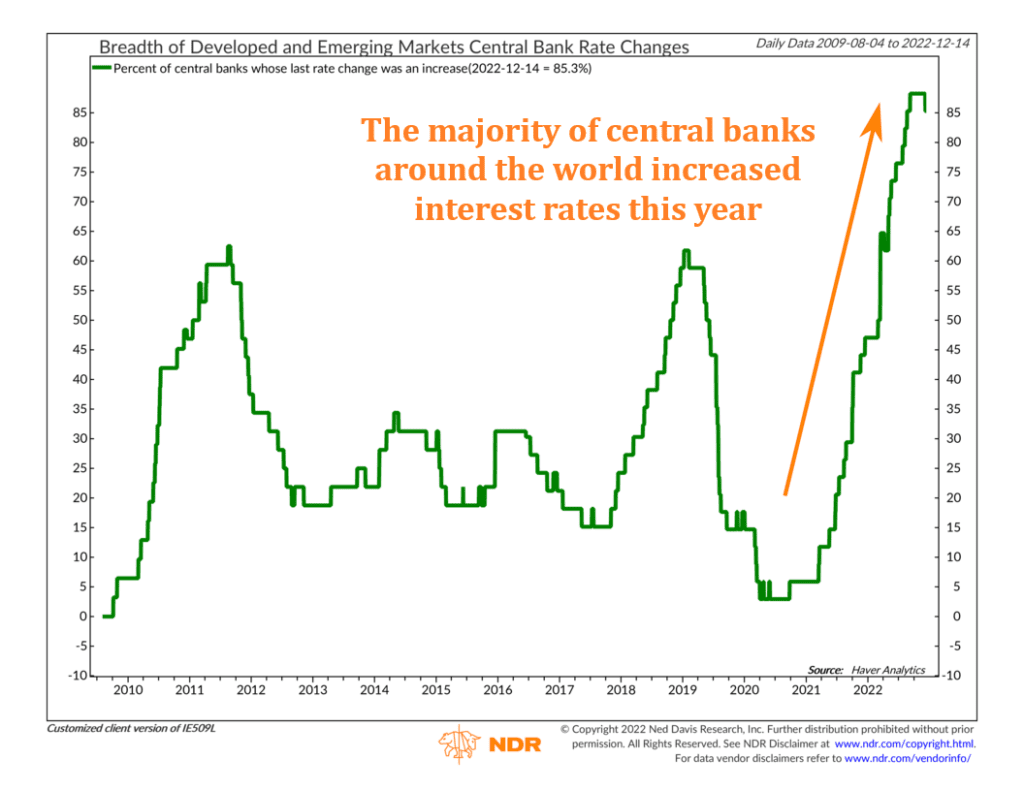

A Hawk on Every Branch – When I look back at the story of 2022, a major theme stands out: hawkish central banks.

But what does it mean to be “hawkish,” exactly? Well, in the world of finance, “hawks” are policymakers who tend to favor higher interest rates in order to curb inflation and stabilize economic growth. These hawkish central bankers are often willing to tolerate some level of economic slowdown to achieve their goals.

Indeed, after years of ultra-low interest rates, most central banks around the world started raising rates this year to curb inflation and stabilize their economies.

The chart below illustrates this dynamic nicely, showing just how hawkish central banks have gotten.

Specifically, it shows that the percentage of central banks worldwide whose last rate change was an increase went from essentially zero in 2021 to nearly 90% in 2022. That’s a dramatic change in global monetary policy in a short time.

And just this past week, we saw a whirlwind of monetary policy decisions in which the Federal Reserve, the Bank of England, and the European Central Bank raised their target rate by 0.5 percentage points. To be fair, this was a slowdown from the 0.75 percentage point moves in recent meetings. But these central banks all went out of their way to avoid declaring a victory over inflation. And going forward, they were all consistent about what would come next: more hawkishness.

So, the bottom line? The good news from all this is that since all the world’s major central banks are working together, it is more likely that the war on inflation can be won. However, the bad news is that this also heightens the risk of global economic distress—which can be bad for stock prices.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The post A Hawk on Every Branch first appeared on NelsonCorp.com.